How EPF Contribution Structure Works

Breaking down the employee and employer contribution rates, how deductions work, and what actually goes into your EPF account each month.

Why Understanding Your Contributions Matters

Your EPF account isn’t just about the money you contribute — it’s about knowing exactly where those funds go and how they work for your retirement. Most employees don’t fully understand the breakdown between what they pay and what their employer pays. That gap in knowledge can lead to surprises down the road.

Here’s the thing: EPF contributions are deducted directly from your salary, so you don’t see the money leave your account. But understanding the structure helps you plan better, know what to expect during withdrawals, and recognize the actual value your employer is putting toward your retirement security.

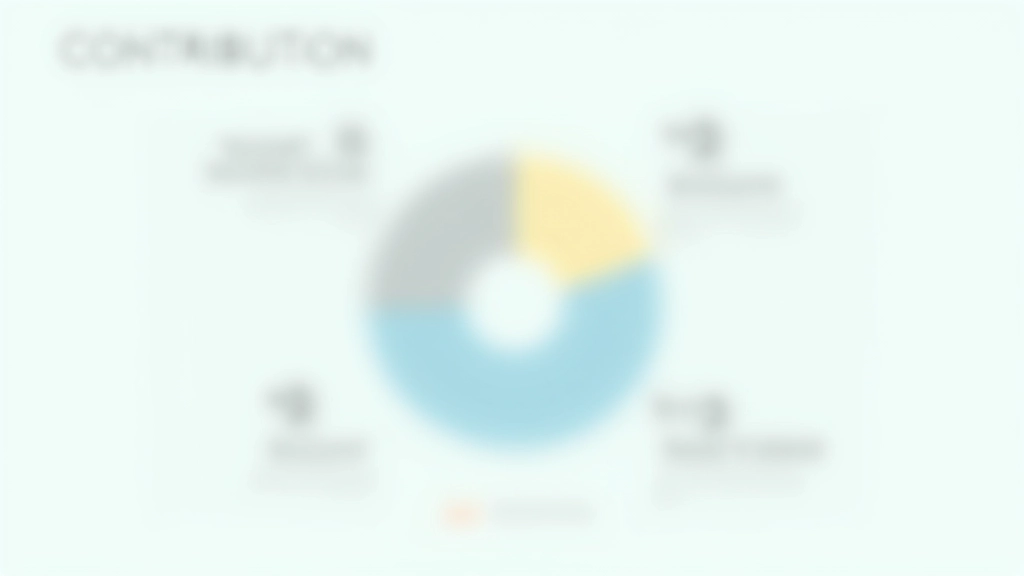

The Basic Contribution Breakdown

EPF contributions are split between you and your employer, and they’re divided into two separate accounts. This isn’t random — it’s intentional design. Account 1 is your main retirement savings, while Account 2 serves as your insurance and disability coverage.

For employees earning up to RM4,000 per month, your contribution is 11% of your basic salary. Your employer matches that with 12%, bringing the total to 23%. It sounds straightforward, but the split between your accounts matters more than you’d think.

Your 11% goes like this: 8% into Account 1 (retirement fund) and 3% into Account 2 (insurance and other provisions). The employer’s 12% gets divided as 11% to Account 1 and 1% to Account 2. So Account 1 actually gets 19% combined (your 8% plus employer’s 11%), while Account 2 gets 4% combined (your 3% plus employer’s 1%).

Understanding Account 1 vs Account 2

Account 1: Retirement Fund

19% CombinedThis is your primary retirement savings. It grows from your contributions plus annual dividend payouts. You can’t touch this money until you’re 55 years old, with very limited exceptions.

- Your 8% contribution

- Employer’s 11% contribution

- Annual dividend distributions

- Withdrawn at retirement (age 55+)

Account 2: Insurance & Housing

4% CombinedThis account covers disability and survivor benefits, plus you can use it for housing purchases before retirement. It’s more flexible than Account 1 but serves a protective function for you and your dependents.

- Your 3% contribution

- Employer’s 1% contribution

- Insurance coverage included

- Can withdraw for house purchase

How Your Deductions Actually Work

Every month, your employer calculates 11% of your basic salary (not including allowances or bonuses in most cases) and deducts it from your pay. You’ll see this on your payslip as “EPF Employee” or “KWSP Pekerja.” The employer then adds their 12% contribution on top, but that doesn’t come from your pocket.

Let’s work through a real example. Say your basic salary is RM3,000. Your monthly deduction is RM330 (11% of RM3,000). Your employer contributes RM360 (12% of RM3,000). That’s RM690 total flowing into your EPF accounts each month — RM570 to Account 1 and RM120 to Account 2.

The deduction happens before income tax calculations, which is actually a tax benefit. Since you’re contributing pre-tax money, your taxable income is reduced. This means you’re getting tax relief on your EPF contributions — another reason understanding the system pays off.

Contribution Rates by Salary Level

The percentage changes if your basic salary exceeds RM4,000, which affects higher-earning employees differently.

Important: For salaries above RM4,000, contributions are capped at the rates shown. So if you earn RM5,000, you’ll still only contribute RM440 (not RM550). This is good news for higher earners — it creates a ceiling on their contributions.

Beyond Contributions: Dividends & Growth

Your EPF balance doesn’t just sit there. EPF invests your money in government bonds, stocks, and other assets. At the end of each year, they distribute dividends back to your account. This isn’t guaranteed, but historically EPF has paid dividends almost every year for decades.

Recent dividend rates have ranged from 5% to 8% per annum, though they vary year to year based on investment performance and market conditions. This compound growth is what makes long-term EPF membership valuable. A small contribution today becomes significantly larger by retirement through this dividend mechanism.

The dividend is automatically credited to your account — you don’t need to do anything. It’s reinvested, meaning next year’s dividend includes returns on the previous year’s dividend. This snowball effect is powerful over 30-40 years of employment.

Special Cases & Exemptions

Not everyone contributes at the standard rates. Here’s what you need to know about exceptions.

New Employees

Employees under 21 contribute 3% for the first 6 months. This is a probationary period that encourages younger workers to join the system gradually.

Self-Employed

Self-employed individuals can voluntarily contribute to EPF. They contribute their own full percentage without an employer match, which is different from traditional employees.

Age 55 & Above

Once you reach 55, you can start partial withdrawals from Account 1. Some employees continue working beyond 55 with modified contribution arrangements.

Housing Withdrawals

You can withdraw from Account 2 for property purchases, which reduces the amount available at retirement but serves immediate housing needs.

Planning With Your EPF Contributions

Understanding how much you’re contributing helps you project your retirement balance. Most people don’t calculate this until they’re much older, but doing it early gives you time to adjust if needed.

The key is knowing that your contributions + employer contributions + dividends = your eventual balance. If you start at age 25 with a RM3,000 salary and get 6% average annual dividends, you’re looking at a substantial amount by 55. But if you only start at 45, the compound growth window shrinks significantly.

That’s why understanding the structure matters. You’re not just watching money disappear from your paycheck — you’re building a safety net that grows with time. Many employees discover they’re actually receiving more value than they initially thought once they break down the numbers.

Important Disclaimer

This article is educational material designed to help you understand how EPF contributions work in Malaysia. The information provided is based on current EPF regulations as of March 2026, but policies and rates can change. For the most up-to-date information, always check the official EPF website or contact your HR department directly. This content is not financial or investment advice — it’s explanatory information only. If you need specific guidance about your personal EPF situation or retirement planning, consult with a qualified financial advisor or contact EPF customer service.

Explore Related Topics